Former Bank of Canada Governor David Dodge said the increase in spending in the federal government’s new budget will make the central bank’s battle against rising prices more difficult.

Sales of previously-owned homes in the US fell in March from a one-year high, underscoring the lingering impact of high mortgage rates and elevated prices.

Blackstone Inc. collected more fees from big retail funds and credit strategies during the first quarter, compensating for the slower pace of deal exits.

Canada’s mortgage lenders are “swamped” as homebuyers rush into the market ahead of new rules that will undercut the average family’s home-buying power.

Ottawa’s latest attempt to take risk out of the housing market will, quite simply, make it harder for Canadians to get a mortgage after this weekend.

“The Department of Finance didn't give homebuyers much forewarning, just two weeks -- and that was by design,” Rob McLister, founder of RateSpy.com, told BNN in an email.

“Most mortgage finance companies are swamped.”

While the new rules officially kick in Monday, McLister suggests it will be hard to find lenders or brokers who can process an application in time if it comes in past Friday.

WEIGH IN: Are you cutting back on discretionary spending due to Canada’s new mortgage rules? https://t.co/GELCo0yTd6

While savvy buyers aware of the new rules are pulling ahead plans to buy a home, others have been blindsided.

“We have found that potential home purchasers, especially first-time home buyers, are stunned that they may now not be able to get a mortgage,” Ajay Soni, president of the Canadian Mortgage Brokers Association, told BNN.

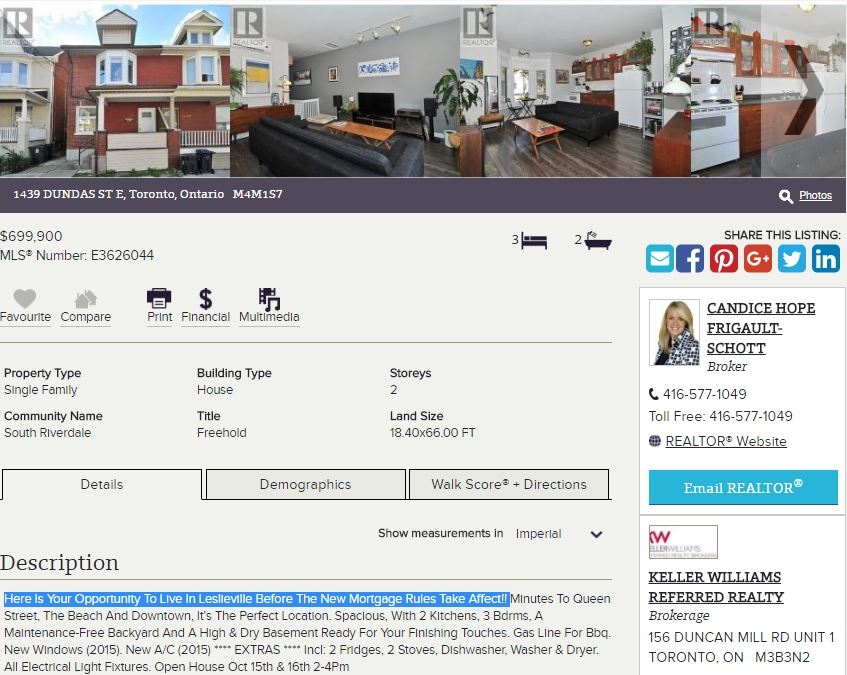

In fact, the spectre of being able to afford far less home as of Monday became part of the sales pitch for one listing in a sought-after Toronto neighbourhood.

“Here Is Your Opportunity To Live In Leslieville Before The New Mortgage Rules Take Affect!!” reads the posting on Realtor.ca for a semi-detached listed at $699,900.

Courtesy of Realtor.ca

The new rules are aimed at insured mortgages. If you make a down payment of less than 20 per cent of the home’s purchase price you’re seeking a high-ratio mortgage, and you need mortgage insurance.

As of Oct. 17, all insured mortgages will be stress tested at a dramatically higher interest rate, based on the Bank of Canada’s posted five-year fixed rate (currently 4.64 per cent).

Here’s what it means for the Canadian homebuyer (example courtesy of Ratehub.ca):

A family with $100,000 of income that saved up $40,000 for a down payment can afford a $665,000 home today. After Oct. 17, when the new stress test rules kick in, that same family can only afford a $505,000 home. That’s a difference of $160,000, representing a 24% drop in affordability.

That’s a considerable hit to a family’s home-purchasing power, and Bruce Joseph, principal of Anthem Mortgage, is seeing an “increased sense of urgency this week to enter the market.”

For its part, Canada’s housing agency says it’s too early to tell what impact the incoming rules are having on home-buying decisions.

“That being said, we have seen in the past some moderate increases in volumes leading up to the implementation of new mortgage rules,” a spokesman for Canada Mortgage and Housing Corporation said in an email to BNN.