Mar 23, 2017

Pattie Lovett-Reid: No more Canada Savings Bonds – who cares?

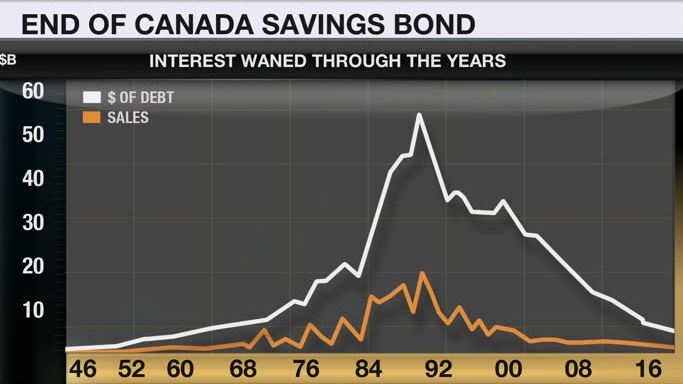

Canada Savings Bonds will soon be a thing of the past. They have been around since 1946, yet haven’t been really competitive for a long time. So what is a saver to do now?

Mortgage rates move higher quickly, but savings rates sure do not seem to move at the same pace. The current rate environment for savers is appalling, add to that a shrinking market, it is no wonder there is a lack of comparison shopping for better rates going on. Not only are we not shopping around, according to a new EQ Bank survey, 45 per cent of Canadians do not even know their savings account interest rate.

Canadians say they want to save more, but are failing to do so given then their lack of awareness on how to get the best rate, or what’s their current rate, in the first place. It gets worse -- Canadians are passive savers. More than three-quarters (77 per cent) of respondents to EQ Banks's survey say they have shopped around for the best telecom deals but only 38 per cent have shopped around for a savings account.

Here are some other stats:

• Millennials (18-34) are most likely to say they have shopped around for a savings account (43 per cent vs. 38 per cent of all Canadians).

• Women are more likely than men to not know their savings rate (48 per cent vs. 55 per cent).

• Those in higher income brackets are more likely to know their rate versus those in lower brackets (60 per cent of those making more than $100,000 know their rate compared to 43 per cent of those making less than $40,000).

We all know there's no science to saving more. Save more than you spend and tuck it away. But if you are serious about savings, you may need to change your habits.

Begin by doing an inspection of all of your accounts and add up all the fees you are paying. Fees diminish returns and with so many options from financial institutions that offer low/no fee accounts it just makes (cents) sense to shop around. As my mother would say, "if you saw $25.00 on the ground would you bend down and pick it up?" You bet I would. Even if the difference is small it is still worth investigating and possibly moving your money for.

Create separate accounts for separate savings goals. Depending on the timeline and the amount you have, you could explore options outside of savings accounts such as Treasury Bills, Money Market Funds and even Bankers Acceptance Notes. Savings are different from investments. Savings are often associated with a goal of protecting the principle at all costs and while you don't expect a lot of return on your investment you want something to help your savings grow.

Dan Dickinson of EQ Bank suggests you do more with your mobile. Mobile banking is all about convenience and can help you save too – use it to transfer money into those savings buckets at the moment you’re thinking about them. For example, unlock your phone and throw a few bucks into your Vacation fund as soon as you start planning a road trip with your friends. You can also push a little into that education fund after finishing your child's bedtime story. Save for what matters to you in accounts (or envelopes!) with names that mean something.”

Forget being passive, it is time for Canadians to get aggressive about saving and don't let the excuse of "low rates" hold you back from getting the biggest bang for your buck. Canada Savings Bonds may be gone but there are other options.