Oct 20, 2017

Why analysts and investors aren’t seeing eye-to-eye on Crescent Point

Crescent Point Energy hasn't lost its shine with the analyst community despite high debt levels, numerous dividend cuts and unexpected share offerings over the past few years. Investors, on the other hand, have punished the stock — sending shares of the former market darling down about 80 per cent from the 2014 high, as fundamentals and sentiment soured in the wake of the oil price collapse.

Yet, analysts are keeping the faith, with 15 “buy” recommendations, six “holds” and not a single “sell.”

Many analysts point to the company's strong asset base as the basis for their continued confidence.

Nima Billou, an analyst at Veritas Investment Research who has a "buy" rating on the company, told BNN in an email he has liked the name for a while because of its focus on oil and natural gas liquids production and the company's ability to quickly adjust its capital expenditures according to the commodity price environment.

“We believe the company can outperform as it can grow its production at least four to five per year even at US$50 [oil], and can fund its capital expenditure budget from cash flows at this conservative oil price in 2018,” he wrote.

TD Securities Analyst Menno Hulshof wrote in a July 27 note to clients one of the main reasons he likes Crescent Point's business model is its high-quality assets, which he thinks have long-term upside.

Analysts seem particularly optimistic about Crescent Point's Uinta operations in northeastern Utah, despite it representing just a fraction of its overall production.

“Additional positive Uinta drilling results lend credibility to an asset that, in our view, remains heavily discounted by the market,” Hulshof wrote.

And Kalvin Baim, a research associate at GMP FirstEnergy, points out Crescent Point’s original five-year production forecast for the Uinta basin was 40,000 barrels of oil equivalent per day, but recent drilling results have nearly doubled that outlook.

Investors, however, haven't been so forgiving.

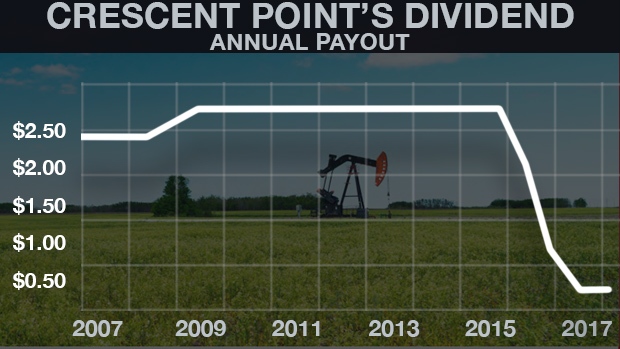

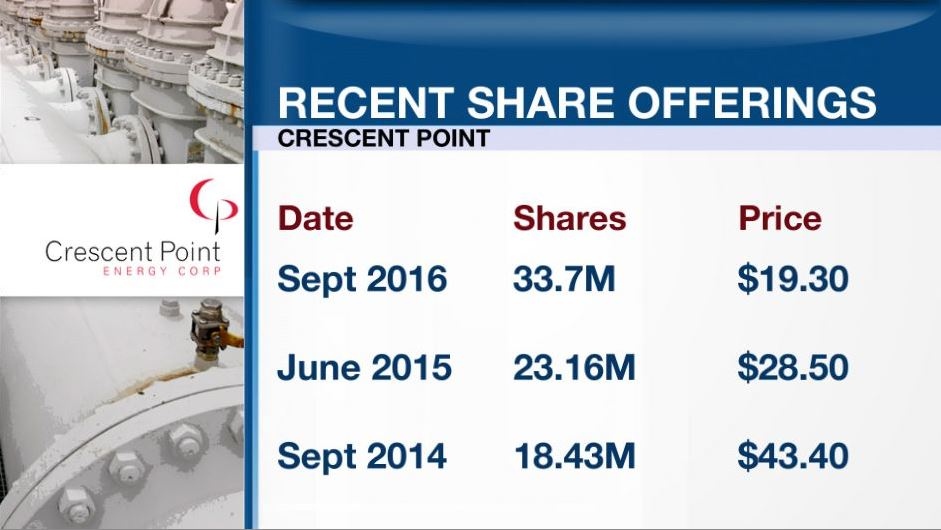

Crescent Point Chief Executive Officer Scott Saxberg embarked on a series of dividend cuts in the face of falling oil prices after saying he wouldn’t do so, and conducted three equity offerings between 2014 and 2016 which some shareholders argue was not communicated properly.

Michael Giordano, vice president of investments at Stone Asset Management, told BNN in an email he owned the stock for several years in client accounts but sold it when investors started pulling money out of the firm's resources fund.

Giordano said the company’s production growth is limited compared to its peers and noted its high debt levels.

He also said some investors likely have complaints about management compensation and the repeated equity offerings, making them reluctant to get back into the stock after being “burned.”

Ryan Bushell, vice president and portfolio manager at Leon Frazer & Associates, who owns the stock in his personal and client accounts, argues something needs to be done to restore trust.

“I rarely say this, but I think this company would benefit from a leadership change,” he wrote in an email to BNN.

“While Scott Saxberg has been instrumental in building a great pool of oil assets, he has also lost credibility with investors by emphatically defending the dividend before cutting it twice and saying he was finished issuing equity, then issuing more last fall. I still believe this company has a future, but something needs to be done to restore credibility.”

While the investment community will get a fresh look at Crescent Point when it reports earnings on October 27, at least one analyst believes investors just need to rethink how this stock is looked at.

“The name should be viewed as a large oil-weighted balanced growth story rather than one where production growth is being used to support dividend growth,” Cormark analyst Amir Arif wrote in a recent note to clients.

“While the company lost some investor confidence in 2016, results from the last two quarters show a meaningful underlying improvement taking place and we would encourage investors to take a fresh look at this name. In our view, [Crescent Point] should be viewed as a large oil-weighted balanced growth story rather than one where production growth is being used to support dividend growth.”

Primrose Lake oil sands project. , REUTERS/Dan Riedlhuber")