Jan 8, 2018

Keith Richards' Top Picks: January 8, 2018

BNN Bloomberg

Keith Richards, portfolio manager at ValueTrend Wealth Management of Worldsource Securities

FOCUS: Technical analysis

_______________________________________________________________

MARKET OUTLOOK

I enjoyed reading Norman Levine’s write-up for his BNN appearance on Dec 28. As Mr. Levine noted, 2017 was an anomaly. Value stocks took a significant back seat to higher beta growth stocks. At ValueTrend, we are not pure value investors. Our strategy combines technical trend and risk/reward measurements such as sentiment and market breadth with “GARP” (Growth at a Reasonable Price) analysis. For us, the anomaly of 2017 was as much about an exuberant focus on overbought growth stocks as it was a complete disconnect from the higher risk market conditions. As with value investors like Mr. Levine, the disconnect from risk was puzzling to those of us who use quantitative risk analysis strategies. As I noted in my last BNN write-up, market breath, volatility and investor sentiment suggested the potential for risk was higher than normal for much of the second half of 2017. Yet the market went up with nary a ripple! To paraphrase Mr. Levine, just because value, or risk-adverse strategies, didn’t perform as well as the “risk-on” trade in 2017, managers who follow such disciplines didn’t suddenly become stupid.

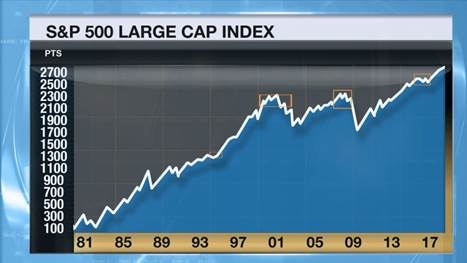

Recently I presented a long termed chart of the S&P 500 on my blog illustrating how markets tend to rotate into a period of higher volatility after an extended period of low volatility. I believe that investors should be prepared for a return to a more volatile marketplace in the coming year. Fear not, though. With volatility comes opportunity. It’s clear that the irrational exuberance surrounding certain growth stocks cannot continue indefinitely. With a return to more rational behavior, there is a strong probability that markets will rotate into many of the currently overlooked stocks and sectors. These overlooked sectors and stocks have been our prime buying focus in recent months, illustrated by my three top picks today.

TOP PICKS

VERMILION ENERGY (VET.TO)

This is an oil and gas producer with properties throughout North America, Europe and Australia. This stock is one of our recently acquired Canadian energy stocks, which we feel are primed to move up. The energy sector has trailed the price of oil and we think it is one of the more overlooked sectors on the market. VET is in the early stages of an uptrend after putting in a bottom just under $40 in 2017. If WTI crude breaks resistance at US$62, VET could reach $60/share as a reasonable target.

BMO U.S. BANK HCAD ETF (ZUB.TO)

This ETF holds the big names in U.S. banks. We bought the ETF a while ago, and it's only just beginning to break out of a consolidation that began in late 2016.

BROOKFIELD ASSET MANAGEMENT (BAMa.TO)

This is the mother ship of the Brookfield enterprises. They hold real estate assets, infrastructure, renewable power and private equity. When you own BAMa you hold pieces of the other listed partnership stocks. Management is focusing on growing their managed asset business. The stock was pretty flat from 2015 to late 2017 so we avoided it. But in the fourth quarter of 2017 it began to break out through $50. With no overhead resistance ahead of the stock, there is significant upside if the fundamentals continue to look strong.

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| VET | Y | Y | Y |

| ZUB | Y | Y | Y |

| BAMa | Y | Y | Y |

PAST PICKS: OCTOBER 31, 2017

VANGUARD FTSE DEVELOPED ALL CAP EX-NORTH AMERICA HCAD INDEX ETF (VI.TO)

- Then: $29.12

- Now: $30.01

- Return: 3.05%

- Total return: 3.48%

FAIRFAX FINANCIAL (FFH.TO)

- Then: $679.41

- Now: $647.76

- Return: -4.65%

- Total return: -4.65%

BMO LOW VOLATILITY CANADIAN EQUITY ETF (ZLB.TO)

- Then: $30.70

- Now: $30.31

- Return: -1.27%

- Total return: -0.62%

TOTAL RETURN AVERAGE: -0.59%

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| VI | Y | Y | Y |

| FFH | Y | Y | Y |

| ZLB | Y | Y | Y |

TWITTER: @ValueTrend

WEBSITE: www.valuetrend.ca