Feb 26, 2018

Personal Investor: How to save on taxes with the right RRSP/TFSA balance

By Dale Jackson

Let’s face it. Most Canadians love their registered retirement savings plans for their immediate tax benefits. Beyond that, it’s a way of saving for some day way off in the future.

But with the contribution deadline just days away, it might be time to visit that future and see how a good strategy can keep the tax savings coming.

The most important thing to know is the RRSP is not a tax-free plan. It’s a tax deferral plan. That means all that money you contribute over the years, and all the money is accumulates as investments will be fully taxed when you withdraw it in retirement. If it grows too much, the tax implications could be staggering.

The trick is to withdraw from your RRSP (or registered retirement income fund) in the lowest tax bracket and ensure any other funds you need come from a tax-free source. Tax-free sources include a tax free savings account, money from the sale of a principal residence, funds borrowed from a home equity line of credit (HELOC), or money in any other non-registered account.

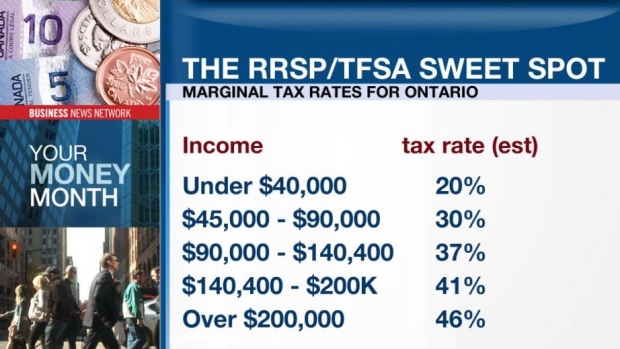

Tax planning always starts with a review of marginal tax rates from the Canada Revenue Agency website. Below is a simplified version to make the point. Imagine you could restrict your annual RRSP withdrawal to $40,000. Your money would be taxed at the lowest rate of about 20 per cent. As you can see, the more you withdraw, the higher the tax bracket.

In a perfect tax plan, any other living expenses would be drawn from a source that isn’t taxed. How much you need depends on who you are, but any untaxed dollar drawn above the lowest bracket comes with at least a 30-per-cent tax savings.