Dec 5, 2017

Retail roundup: What to watch as Dollarama, HBC, Lululemon report

A trio of very different Canadian retailers are set to report third quarter earnings Wednesday, giving investors a view into their operations heading into the key holiday season. Hudson’s Bay Company and Dollarama results will hit the tape before the opening bell, while Lululemon will report shortly after the close. Investors will be watching a number of key, but disparate, metrics for signs of how each of the three are faring.

Dollarama (DOL.TO):

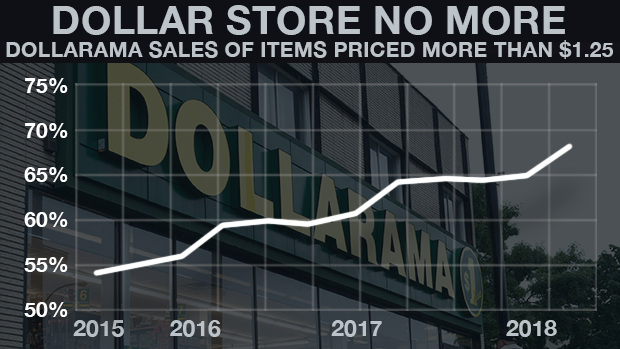

Dollarama is quickly becoming a dollar store in name only. The discount retailer has been leaning more and more on sales of items costing more than $1.25 apiece, which now accounts for more than 68 per cent of sales, up from just 54 per cent in the third quarter of 2015. Combined with its acceptance of debit and credit cards across the chain, the average size of each transaction has risen, albeit at the expense of foot traffic as customers load up on fewer trips.

Analysts have taken note of the higher average sale price. In a Nov. 28 research note to clients, Eight Capital equity analyst Tal Woolley said he expects the higher prices will help drive revenue growth as new store openings slow. Woolley has the equivalent of a “buy” rating on the stock and a 12-month target price of $185.

“Today, when we visit stores, we are still consistently impressed by the diversity of merchandise, the value on offer (e.g., apart from appliances, you can now outfit an entire kitchen at [Dollarama] at a fraction of the cost of a specialty store), and most importantly, the customer lines,” he wrote. “Simply put, customers see the value in the higher price-point goods.”

On average, analysts are expecting Dollarama to report $1.11 in earnings per share on revenue of $824 million, according to data compiled by Thomson Reuters. The stock has 12 buys, six holds and zero sell ratings, with an average target price of $157.41.

Hudson’s Bay Company (HBC.TO):

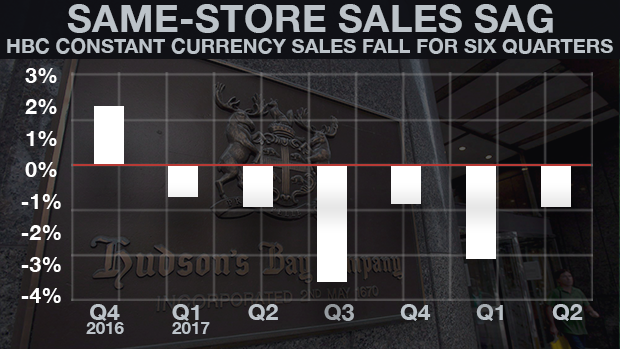

The investment community is eagerly anticipating more information on a pair of fronts from Canada’s oldest retailer. Investors want further clarity on the company's plans to unlock the value of its vast real estate holdings, which it estimates to be worth as much as $35 per share as well as how it hopes to reverse the sagging sales of stores open for more than a year. Same-store sales have declined in each of the last six quarters, when adjusted for currency fluctuations, as customers increasingly head to online retailers like Amazon for their shopping needs.

A harsh hurricane season could also crimp results, according to BMO equity analyst Wayne Hood. In a Nov. 14 note to clients he said HBC’s exposure to hurricane-stricken markets could weigh on sales growth. Hood has the equivalent of a “buy” rating on the stock with a $25 12-month target price.

“Florida accounts for roughly 11% of HBC's U.S. store-base, and Texas ~7%, so we factor in a modest headwind to [third quarter same-store sales,] which coupled with the sales trends reported throughout the industry, prompt us to lower our [estimate to a] 1.9% [decrease,]” he wrote.

On average, analysts are expecting HBC to report a $0.74 loss per share for the quarter on revenue of $3.41 billion, according to data compiled by Thomson Reuters. The stock has two buys, seven holds and two sell ratings, with an average target price of $14.46.

Lululemon (LULU.O):

Shares of the athleisure company have been steadily improving into the end of the year, after taking a significant hit in March when the company reported weaker-than-expected earnings. The company has been diversifying its product base, expanding further into footwear and men’s clothing in a bid to increase its appeal outside of its traditional yoga-obsessed cohort. In a Nov. 30 note to clients, Barclays equity analyst Matthew McLintock expressed enthusiasm about the growth prospects for the menswear division. Barclays has the equivalent of a “buy” rating on the stock and a US$85 12-month target price.

“During the quarter the company launched a significant amount of new product including a new fabric innovation, as well as an expanded assortment within the ABC [men’s pants] franchise,” he wrote. “We believe men’s [clothing] will show strength in [the third quarter] as reception of the new product was positive, and because the company launched its first-ever global men’s campaign in September.”

On average, analysts are expecting Lululemon to report US$0.52 in earnings per share on revenue of US$610 million, according to data compiled by Thomson Reuters. The stock has 17 buys, 14 holds and two sell ratings, with an average target price of US$67.89.