Feb 19, 2020

MoneyTalk: Stashing your cash

Presented by:

![]()

Where to put the extra money

Maybe you’ve checked your cash flow, and identified some extra money in your monthly budget to sock away, or maybe you’ve gotten a commission or bonus from your employer and are looking to put it aside for a rainy day. How do you decide where it goes? Stephen Inskip is a Regional Vice President of Financial Planning at TD Wealth. He offers some options when choosing the right place for your savings.

Retirement Savings Plan (RSP)

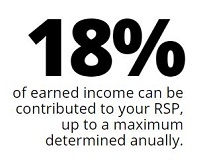

An RSP is a tax-deferred investment account which allows you to grow your savings for retirement. When you contribute to an RSP, your contributions can be used to reduce your taxable income, but you may face taxes when you choose to withdraw from the RSP. There is no tax on any gains or investment income while the assets are held within the RSP. You can hold different types of assets in an RSP, like equities, bonds, most mutual funds and may be able to hold other investments that qualify under the Income Tax Act. There is also an annual contribution limit which is based on a percentage of your earned income that accumulates year after year, subject to certain adjustments.

Consider If:

Consider If:

- You are saving for retirement.

- You are saving to purchase your first home, as the RSP Home Buyers’ Plan allows you to withdraw money from your RSP to purchase your first home, subject to eligibility and conditions.

- You are between 18-71 years of age and you expect your income to be lower in retirement than when you were working.

Tax-Free Savings Account (TFSA)

A TFSA is an investment account in which gains and investment income are not taxed when earned in the account, and are not taxed when withdrawn. Each year the government designates a limit for contributions and that room accumulates year after year. A TFSA can hold many different types of investments provided they qualify under the Income Tax Act, such as cash and GICs, stocks and bonds, along with mutual funds and ETFs. You have to be 18 years of age or older to open one.

Consider If:

- You are over the age of 71, as an RSP must be converted to retirement income by the end of the calendar year in which you turn 71.

- You expect to have a sizeable pension or a sizeable income upon retirement, for example more than the Old Age Security claw-back threshold.

- You are establishing a short-term savings account or an emergency fund.

- You want to diversify your retirement income to take advantage of government benefits or tax credits when you retire.

Non-Registered Investment

Non-registered investments are taxed in different ways. Interest income is fully taxable as personal income. Half of capital gains is taxable as income and dividends from Canadian sources are “grossed up” and then subject to a dividend tax credit. Dividends may be more tax-efficient than interest income. There are no contribution limits.

Consider If:

- You have already reached, or are close to the contribution limits on your registered accounts.

- You have already reached the contribution limit on your TFSA and expect to be in a higher tax bracket on retirement than your working years.

Other Options:

RESP (Registered Education Savings Plan)

If you are planning to pay for or contribute to your children’s higher education, consider putting some of your extra money into an RESP. The federal government will contribute an additional 20 per cent on annual contributions of up to $2,500, up to a lifetime grant maximum of $7,200 per beneficiary. Additional grants may be available to lower and middle income families.

Pay Down Your Mortgage

There is no hard and fast rule about saving versus paying down debt, like a mortgage. If you are trying to figure out which should be a priority, consider the interest rate you are paying on your mortgage, and the rate of return you are getting on your investments. Given the current low interest rate environment, if you think you can reap a higher rate of return from an investment, whether it be stocks or mutual funds, you may consider using the money to invest rather than paying off your mortgage. However, if you believe it may be difficult to get a rate of return that is higher than your mortgage rate, then paying off your mortgage may be a prudent choice.

There are many considerations when deciding where to put your money, and everyone’s priorities and situations are different. So talk with a financial professional who can help you weigh your options. You’ll need to consider your financial goals, whether they are short-term or long-term, market conditions, and your tolerance for debt and risk. And ideally, your final decision may come down to which goals or priorities are more important to you.