Nov 24, 2017

Mortgage stress tests and U.S. growth: What to watch in bank earnings season

By Paul Bagnell

The last time Canada’s big banks reported quarterly earnings, investors went on a bank-stock buying spree that propelled the shares dramatically higher – taking the S&P/TSX Composite along for the ride.

Since those third-quarter results – the last set of which landed on Aug. 31 – Canada’s banks have returned a remarkable 12 per cent to shareholders and the S&P/TSX has returned eight per cent.

With fourth-quarter results set to start rolling out on Tuesday, there are two burning questions for investors:

Can the banks top expectations again?

And can shares surge again on the back of those results?

Yes.

And no.

That’s the view of analysts who cover the sector.

“All things considered, we would not be shocked to see yet another quarter of positive earnings per share surprises,” wrote Gabriel Dechaine, who covers the banks for National Bank of Canada, in a recent report to clients. “However, with the banks outperforming the market by about 450 basis points since reporting fiscal third-quarter results, we believe upside into the quarter is limited.”

Scott Chan at Canaccord Genuity also sees the banks topping estimates in the quarter – and is slightly more constructive on where share prices are going. After the strong third-quarter results, he raised his target price-earnings multiples on the stocks slightly – to 12.75 times expected yearly earnings from 11.75 times. But he says it may take a year for that multiple expansion to take place. The banks are trading at 11.9 times expected earnings right now.

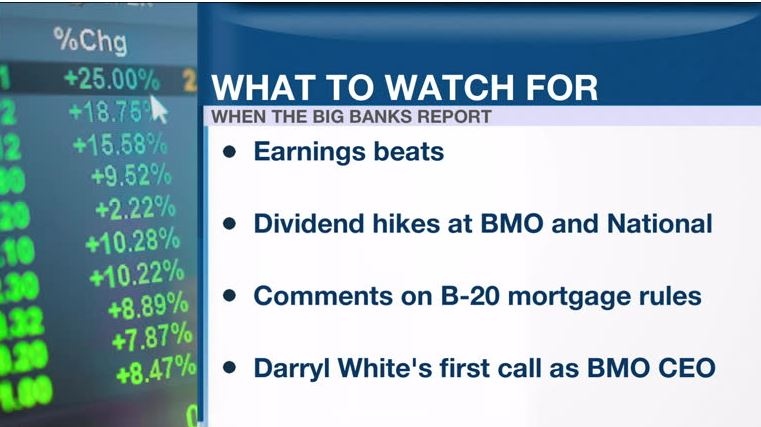

Here are some themes to watch for:

- Earnings per share growth of five or six per cent versus the fourth quarter of 2016, with most banks topping street expectations. Earnings growth will come from solid results in Canadian retail banking, low levels of loan losses, strong growth in wealth management profits and the ongoing effort to control costs. Weakness is expected to come from the trading desks. The big U.S. banks all reported disappointing trading in fixed income, currencies and commodities (FICC) and that trend is expected to be echoed here in Canada.

- Dividend hikes for shareholders of Bank of Montreal and National Bank of Canada.

- Insight from bank executives on the impact of Ottawa’s new mortgage-underwriting rules, which come into effect on January 1, 2018. Known as Guideline B-20, they require stricter stress tests on uninsured mortgages and tougher loan-to-value limits -- and have the potential to constrain mortgage growth at the banks in fiscal 2018.

Dechaine says this is the quarter’s biggest wildcard. “We believe many investors view revised B-20 rules as a trigger to cause mortgage growth to tumble,” he told clients.

- The state of Bank of Montreal’s U.S. segment. In a document filed with U.S. regulators, BMO said it saw commercial loan growth expand nine per cent during third calendar quarter of the year. Analysts are divided on whether they think this will flow through to meaningful U.S. loan growth in BMO’s fiscal fourth quarter, which ran from the beginning of August through the end of October. If it does, it could mark a turnaround in lackluster U.S. loan growth at BMO.

- Any insight from BMO’s new CEO. This will be Darryl White’s first quarterly conference call as the bank’s chief executive officer. He won’t declare any abrupt shift away from predecessor Bill Downe’s strategic direction, but anything he says on strategy will be keenly dissected. In particular, does he think this is the right time for BMO to make an acquisition to add to its U.S. banking business?

- A clearer view of CIBC’s new U.S. bank. A year ago, Donald Trump’s election sent U.S. bank stocks soaring and forced CIBC to pay more than it had intended to acquire PrivateBank of Chicago. The larger price tag makes the performance of PrivateBank all the more important. Canaccord Genuity’s Chan said the Chicago bank underperformed in the last set of results – but noted those results included only 39 days of PrivateBank as part of CIBC. This time around, investors will see a full quarter’s worth of performance.

Here are the reporting dates for each of the banks, and – according to Thomson Reuters – what analyst expect to see in earnings per share:

- Bank of Nova Scotia (Tuesday, November 28): $1.66 EPS expected, up 5.3 per cent from the fourth quarter of 2016.

- Royal Bank of Canada (Wednesday, November 29): $1.87 EPS expected, up 10.7 per cent.

- Toronto-Dominion Bank (Thursday, November 30): $1.39 expected, up 13.7 per cent.

- Canadian Imperial Bank of Commerce (Thursday, November 30): $2.50 expected, down 0.5 per cent.

- National Bank of Canada (Friday, December 1): $1.38 expected, up 11.1 per cent.

- Bank of Montreal (Tuesday, December 5): $1.19 expected, down 5.2 per cent.

and Bill Downe (right)., Courtesy of BMO")